The number of adviser firms has fallen by 15% since 2021 although the number of advisers overall has remained steady at 31,000.

Consolidation has driven a move towards fewer but larger advice firms on average, according to the FCA’s latest Financial Adviser Survey which 4,100 firms took part in and is published today.

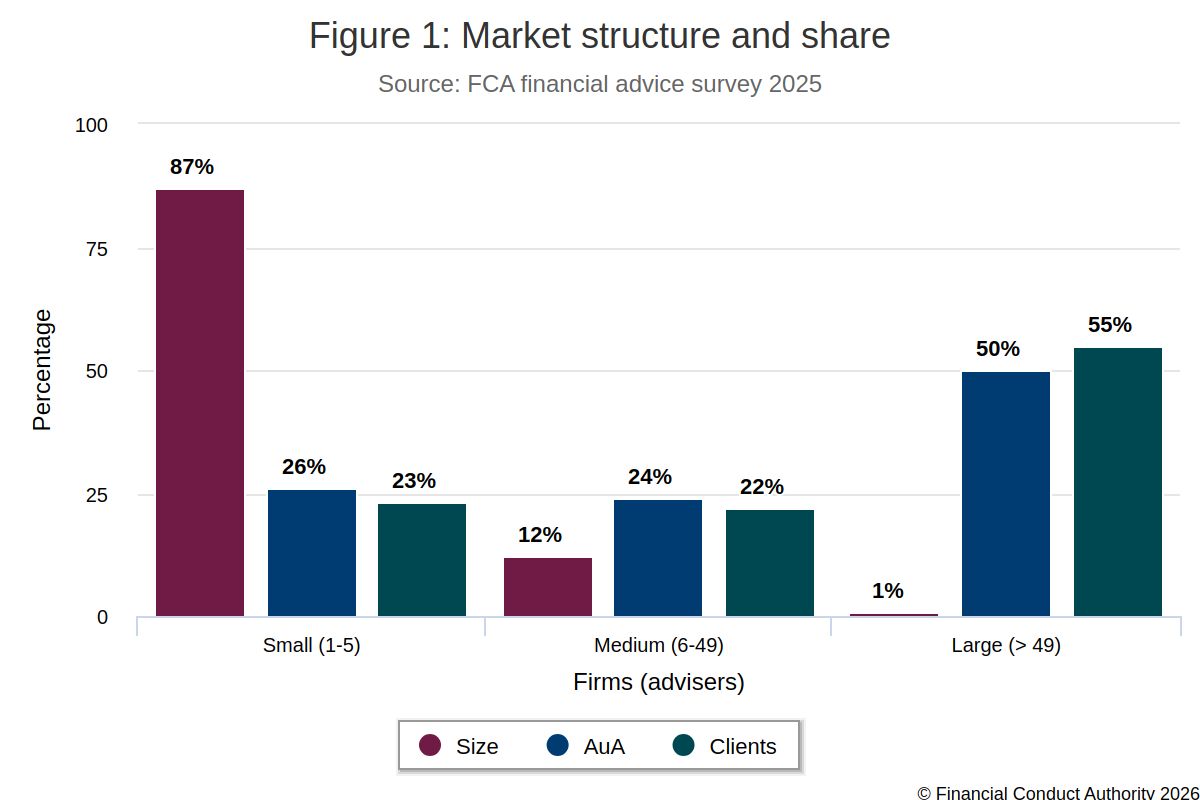

The findings suggest a shrinkage in adviser firm numbers but with the average adviser firm growing in size and employing more advisers on average. Despite the move to larger firms small firms with one to five advisers and medium-size firms remain an integral part of the sector.

The FCA study predicts a further decline in adviser firm numbers by about 5% between now and 2028 - a drop of about 250 - although adviser numbers are likely to remain steady as consolidation continues. Overall there are 5,100 adviser firms offering financial advice.

The FCA said in its report: “We also asked firms about their future growth and contraction plans over the next two years. The analysis of these responses alongside recent trends in newly authorised firms suggests a further reduction in the number of firms of 5% is likely by 2028. There is no evidence though to suggest there will be a reduction in the number of financial advisers.”

The FCA used its survey, along with analysis of data it already holds on around 31,000 advisers.

The FCA said: “Overall, it (the survey) shows a market that remains broadly stable and continues to support millions of clients, even as firms adapt to consolidation, new business models and technology.”

Large advice groups, those with over 50 advisers, form just 1% of firms but provide advice on half of all client assets while "a long tail" of smaller firms continue to serve a wide and diverse client base, the FCA said.

Consolidation continues to reshape the market and around a third of the largest firms are looking to acquire another firm or its client bank in the next 2 years.

Key survey findings include:

- Firms responding to the survey advise on around £1 trillion of assets for more than 4.1 million clients

- Large firms account for around 50% of assets under advice but small firms remain important

- Adviser numbers have remained broadly steady at around 31,000 since 2023, despite a 15% fall in the number of authorised advice firms since 2021. This points to consolidation across the market rather than a reduction in advice provision

- Women account for around 18% of financial advisers, despite being part of around 60% of advised client relationships

- Financial advice remains concentrated among older and wealthier consumers, with regulated advice currently reaching only around 9% of UK adults.

- Nearly a third of firms are considering offering a form of simplified advice propositions to help expand access, particularly for mass affluent consumers.

The survey also showed positive engagement with the Consumer Duty, the FCA said, particularly in pensions and retirement advice, which account for 69% of clients’ main advice objectives.

In terms of gender there is a disparity between Financial Planning and Paraplanning, according to the survey. The survey found that 1 in 5 advisers were female but 1 in 2 Paraplanners were female and 70% of support roles overall were taken by women. Overall, 29% of individual clients were female and 31% of women were part of an advised couple or partnership.

The average age of advisers appears to be falling with 50% of advisers now under 50 and the proportion under 40 rising since 2023.

While number of clients and average assets per client vary widely, a typical adviser profile shows: 150 clients per adviser, £250,000 assets per client and about £2,000 in revenue per client.

• FCA Adviser Market Survey https://www.fca.org.uk/data/understanding-financial-advice-market

• Financial Planning Today Analysis: This comprehensive FCA adviser survey provides a detailed health check on the adviser market. It shows the sector is evolving and remains in robust health generally but there are some causes for concern. The number of adviser firms is well down on five years ago and is set to decline further. Adviser numbers too, despite the potential demand, are stable but not growing. Financial advisers remain responsible for huge amounts of wealth and consolidation in the sector is driving the emergence of larger, more influential advice firms but the lack of growth in adviser numbers suggest there is much more to do to stimulate growth. With only 9% of the population taking professional and regulated financial advice it is clear that the ability of the current advice sector to meet potential demand is very limited. It will be interesting to see if the emergence of Targeted and Simplified Advice will do anything to improve adviser numbers. The FCA has rightly highlighted the positive and important aspects of the advice sector and its shortfalls. With its new growth agenda, perhaps now is a good time for the FCA to encourage the formation of more financial advice firms and the growth of the financial adviser profession. Without more advisers and advice firms it is difficult to see how human financial advisers can serve millions more people and create a better advised population.