Lower costs for housing and household services spurred a substantial fall in the CPI 12 month inflation figure from 3.3% in March to 2.8% in April - although experts have warned the reprieve may only be temporary.

On a monthly basis, CPI increased by 0.7% in April, compared with a rise of 1.2% in April 2025.

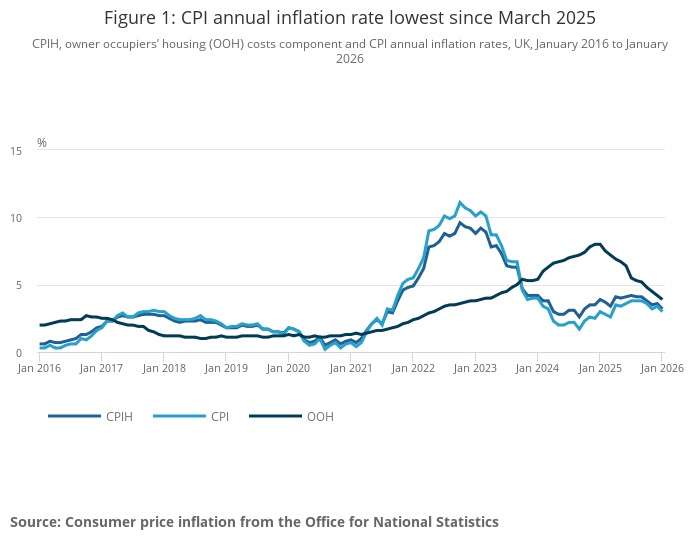

The CPI rate was the lowest since March 2025 and continues a mostly downward trend since the beginning of 2025.

ONS said that housing and household services formed the largest downward contribution to the latest monthly change in CPIH and CPI annual rates.

Upward pressure came from a big increase in motor fuel prices but this was counteracted by downward effects from other categories in the transport division.

The Consumer Prices Index, including owner occupiers' housing costs (CPIH), rose 3.0% in the 12 months to April 2026, down from 3.4% in the 12 months to March.

Core CPIH (CPIH excluding energy, food, alcohol and tobacco) rose 2.8% in the 12 months to April, down from 3.3% in the 12 months to March. The CPIH goods annual rate rose from 2.1% to 2.4%, while the CPIH services annual rate fell from 4.3% to 3.4%.

Core CPI (CPI excluding energy, food, alcohol and tobacco) rose 2.5% in the 12 months to April, down from 3.1% in the 12 months to March. The CPI goods annual rate rose from 2.1% to 2.4%, while the CPI services annual rate fell from 4.5% to 3.2%.

The 12 month rate of RPI, an older inflation measure, fell from 4.1% to 3.0%.

Industry reaction was one of relief but with concern for the future against a backdrop of Middle East conflict.

Charlie Ambler, co-chief investment officer and partner at wealth management firm Saltus, said: “Headline inflation has eased to 2.8% in April, reversing the uptick recorded in March. This is largely driven by favourable base effects, with electricity and gas price inflation expected to have fallen, alongside food and services inflation.

“While the first slowdown of the year will provide short-term respite for markets, significant uncertainty remains. The risk of renewed pressure later in 2026 cannot be ignored, with the Bank expecting inflation to climb to 3.7% by the end of the year. However, much of this depends on how long the conflict in Iran endures and oil prices remain elevated.

“Despite inflation far exceeding target, policy remains finely balanced. The focus for the Bank is the trajectory of services inflation and pay growth. If those measures continue to ease, rate cuts still remain possible in due course, albeit cautiously.

George Brown, senior economist at Schroders, said: "Inflation took a step back in April, but is set to leap at the end of spring. Higher energy prices look likely to lift inflation above 4% this year, having previously been on course to fall to around the 2% target this summer.

"What matters now is whether this starts to bleed into broader price and wage setting. A softening labour market and fragile growth should limit that risk, but the Bank of England can ill afford to be complacent after years of successive global supply shocks. This should keep the Bank sounding hawkish, but we think it will ultimately stop short of hiking rates."

Scott Gardner, investment strategist at JP Morgan Personal Investing, said: “The fall in UK inflation during April was better than expected but it shouldn’t mask the underlying price pressures in the economy. Services inflation in particular has dropped significantly, largely because the hikes to National Insurance and minimum wages we saw last April were not repeated on the same scale this year.

“While this is welcome progress, the month-on-month data arguably offers a clearer read on the UK prices. The spike in energy costs since the war in Iran broke out continues to persist and is being felt harshly by households and businesses. As a result of this, there has been a jump in input prices across both manufacturing and services industries. While some costs have been absorbed by firms, output prices have increased.

“This mixed picture underscores the challenge for the Bank of England and policymakers. Energy and food inflation remains sticky even as services inflation and wage growth shows signs of cooling. This challenge is being compounded by an uncertain geopolitical backdrop in the Strait of Hormuz with the conflict’s inflationary impact starting to be felt beyond energy price rises. Markets are currently expecting two rate hikes later this year but there are too many unknowns right now, making any decision on future rate moves far from clear cut just yet.”