The Treasury's consultation on its proposed new First Time Buyer ISA (FTB ISA) - to replace the Lifetime ISA (LISA) - promises simplicity and closer alignment with the rules on other ISA products.

Unlike the LISA, which could be used for retirement planning, the FTB ISA will solely be for the purpose of buying a first home.

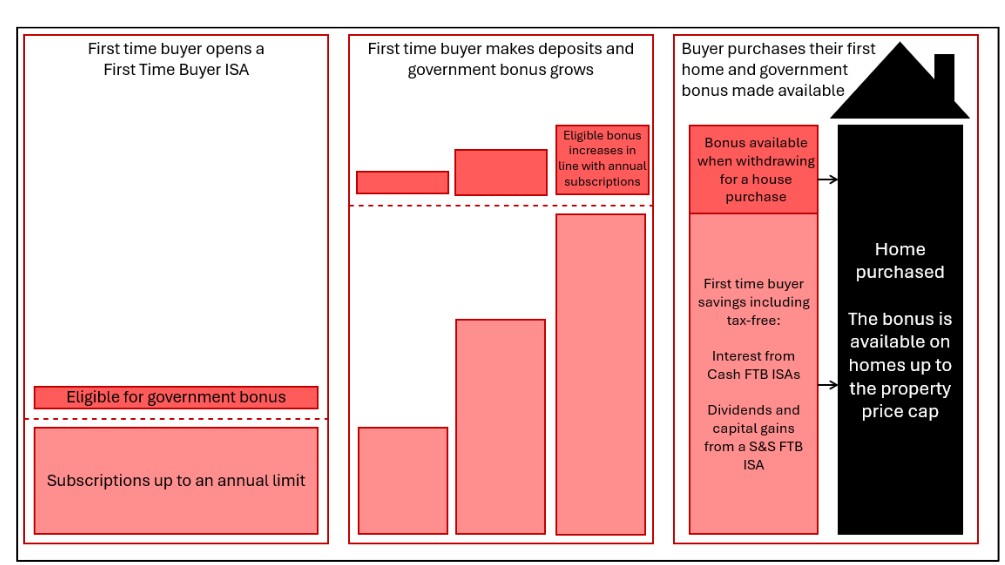

The FTB ISA will include a Government bonus paid at the point of withdrawal, removing the need for a withdrawal charge. It will not be available for cash-only purchases or unregulated financing arrangements.

While the figures have yet to be shared, the FTB ISA will set a price cap on homes it can be used to purchase as well as annual contribution limits. It will also operate as part of an individual’s overall ISA allowances.

The Treasury consultation said that it would like to see both Cash and Stocks & Shares versions of the FTB ISA.

Rebecca William, Financial Planning divisional lead at Rathbones, welcomed the removal of the withdrawal penalty.

She said: “The Lifetime ISA tried to serve two masters - helping people save for a home and for retirement - and in doing so it often created confusion rather than clarity.

“A more focused product that is solely geared towards getting on the housing ladder should be easier to understand and use in practice, particularly as it removes the withdrawal penalty that proved so contentious with the LISA.”

She added that the FTB ISA does not remove affordability issues which are putting a growing strain on many.

She said: “While a simpler savings vehicle is a step forward, it doesn’t change the fundamental challenge facing first-time buyers. Younger generations are contending with a double squeeze of high rents and elevated living costs, making it increasingly difficult to build a deposit. As a result, the traditional milestone of home ownership is drifting into the mid‑thirties for many.

“That in turn is placing growing strain on the Bank of Mum and Dad, with many parents stepping in to help their children onto the ladder - often at the expense of their own financial plans. These pressures are particularly acute for the sandwich generation, who are balancing day‑to‑day costs while supporting both children and ageing parents. Our research shows that 60% expect to delay retirement as a result.”