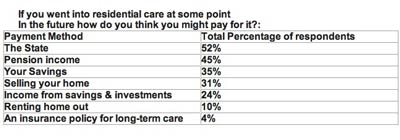

Only 4% would use an insurance policy for long term care. The Partnership Care Index conducted 1023 online interviews with consumers aged over 45, including 100 interviews with those aged 75 and over, to measure attitudes towards long-term care across the UK.

The majority of the consumers questioned (52%), said that they expect the State to fund residential care at least in part, and 45% would use pension income to help with the funding. 31% would sell property outright to fund any long-term care and a further 10% would rent their property to give an on-going income.

Chris Horlick, managing director of care, Partnership, said: "Despite the downturn in the property market, the realisation that property is likely to be a key source of funding for any care costs is becoming more widespread. Estimates suggest that over 65s have unmortgaged equity of nearly one trillion pounds.

As costs of long-term care increase more retirees are struggling to find methods to fund care aside from utilising assets such as property. We believe that greater awareness of the benefits of Equity Release to fund care, will provide another vital source of income for those people who wish to use property to do so.

We also believe that Immediate Needs Annuities, which provide insurance to meet the costs of care will play a far larger role in due course. At present few people are aware of these products, which guarantee an income for life to meet the costs of care in return for a one off premium. The residue can be left as a gift to friends and family. They provide peace of mind for the policyholder and family. If the Government's imminent Social Care White Paper provides a greater focus on information and advice for people seeking to fund the costs of care - this will inevitably stimulate greater awareness of these important financial products."

The Partnership Care Index has been created to measure the attitudes of consumers towards long-term care across the UK.

1023 online interviews with consumers aged 45 and over were carried out, including 100 interviews with those aged 75 and over. Quotas were set on age and gender, and a regional split was ensured.