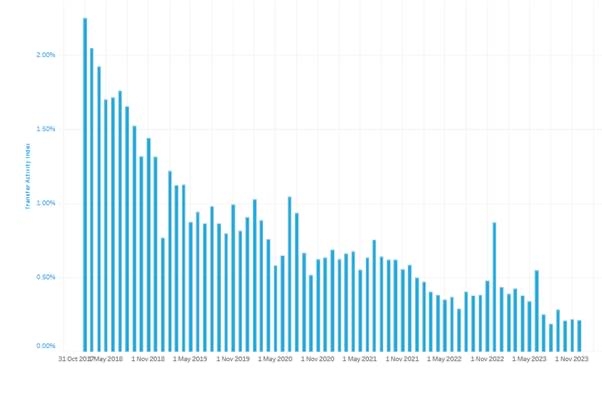

The DB Pensions Transfer Value Index compiled by XPS Pensions increased by 2.6% during November to £156,000, the biggest increase seen since March.

Scotland has introduced a new tax band set at 45% of earnings between £75,000 and £125,140.

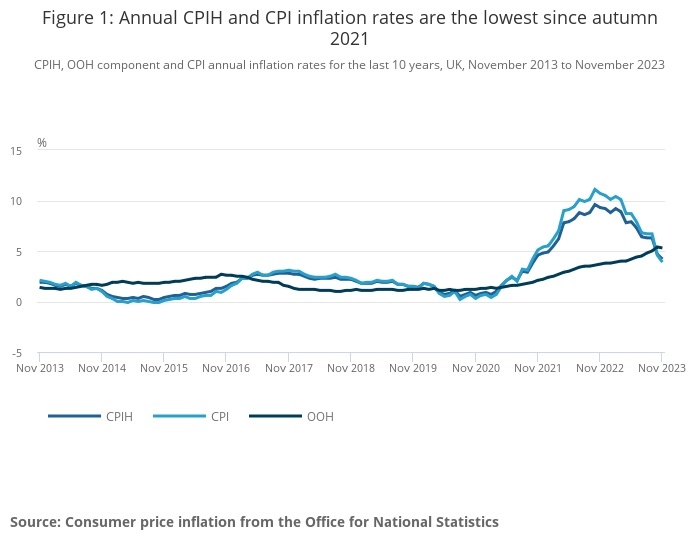

The CPI inflation rate dropped from 4.6% in October to 3.9% in November, continuing a rapid decline seen in recent months.

The FCA has warned that it will intervene on the sale of client banks if selling firms fail to make clear any redress liabilities.

Fintech and data provider Defaqto has unveiled new independent Consumer Duty Profiles for the top 20 most-frequently recommended discretionary MPS portfolios.

Adam & Company, the specialist Scottish wealth management firm and private bank, has hired Financial Planner Kevin Motion from Abrdn to help with its Financial Planning growth plans in Scotland following the acquisition of Glasgow-based £220m AUM Financial Planning firm Intelligent Capital in November.

The CISI has appointed Emma Black Chartered FCSI, co-founder and CEO of Cascade Cash Management, as its new President of the CISI North East Committee.

Financial planning-led wealth manager Atomos is continuing on the acquisition trail with the takeover of two regional advice firms.

A major new research report has revealed that white middle class men from higher socio-economic groups are 30 times more likely to succeed in financial services than working class, ethnic minority women.

Chartered Insurance Institute CEO Alan Vallance is to leave the organisation about three months earlier than planned.