Wealth manager and Financial Planner St James’s Place (SJP) has upgraded its financial crime defences with an Artificial Intelligence (AI) solution.

Lancashire-based Financial Planning firm Breaks Wealth Management has become the latest firm to be hit by clone scammers creating a fake replica of the firm’s website.

Fast growing Financial Planning group Kingswood is planning eight more adviser firm acquisitions in the UK and Ireland this year after unveiling strong revenue growth.

Funds under management dropped 4.8% year-on-year to £15.7bn for wealth manager and Financial Planner Brooks Macdonald for year ending 30 June.

Parmenion Investment Management, the investment arm of adviser platform Parmenion, has added an ESG-focused passive investment solution.

Frenkel Topping, a specialist advice firm focusing on personal injury and clinical negligence cases, has acquired two firms in the care and case management sector.

STM Group, parent company of SIPP provider Options, has reported a 44% drop in profit before tax for the six months ended 30 June.

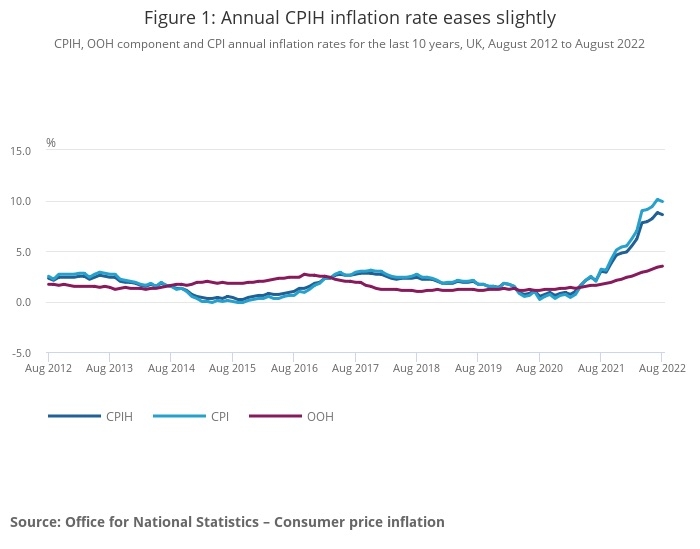

CPI inflation dipped unexpectedly in August to 9.9% from 10.1% in July, according to the latest figures published by the ONS today.

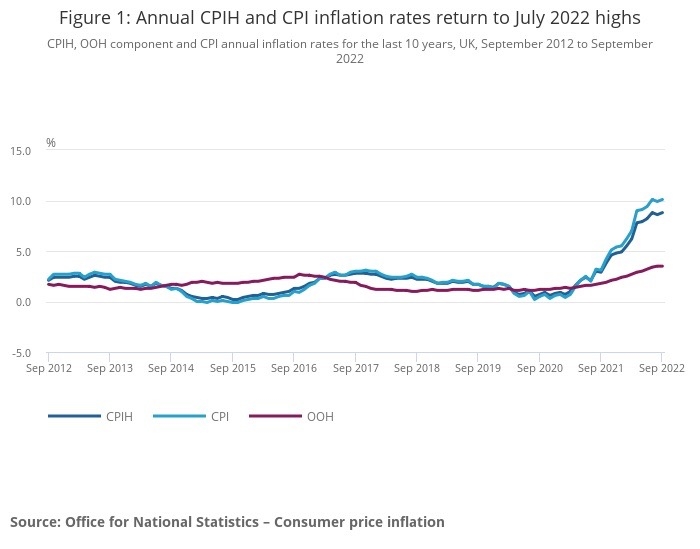

CPI inflation returned to its upward trend in September, hitting 10.1% after a dip in August to 9.9%, according to figures released today by the ONS.

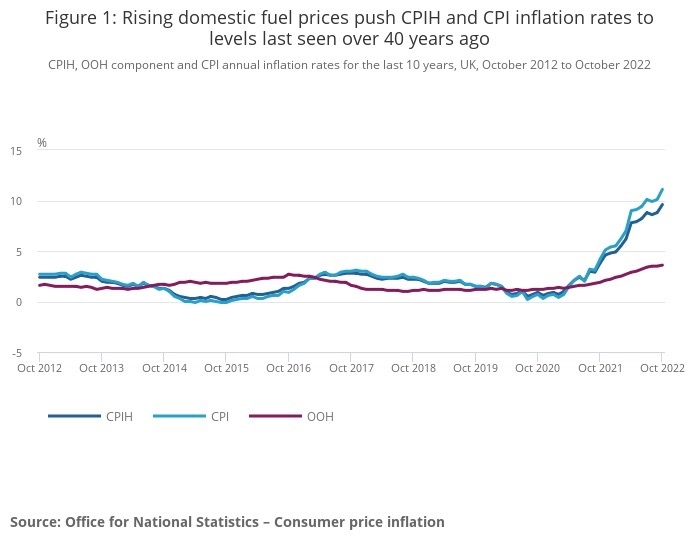

The Consumer Prices Index rose to a 41-year high of 11.1% in October as prices rose in many sectors, with warnings of potential further rises to come.